By Luc de Leyritz | Co-author: Sam Cash

At Project A we believe there’s a meaningful opportunity for large scale businesses to be created in the B2B fintech space by a) streamlining time-consuming workflows which are currently performed manually by the finance team and b) increasing the penetration of these tools in the European SMB market.

There are about 23m SMBs in Europe, all of whom have to manage their finances. However, most don’t use specialised software. Accounting software is a good proxy: despite being the key software piece for a finance team, less than 50% of UK’s SMBs use a software solution for accounting. We believe a) penetration of financial software other than accounting solutions to be much lower and b) that figure to be lower in other European countries than in the UK (where digital reporting is now mandatory for SMBs).

Additionally, the current software offering is mainly legacy software. Most European SMBs use local champions (Datev for Germany, E-conomic in the Nordics, etc…) which can date to the ’60s. In most markets, 80% of SMBs using accounting software use Sage, Quickbooks or Xero, which have been around for an average of 31 years. Excel, the horizontal software which is still the backbone of the economy, and where most data consolidation and reporting tasks happen, is 34-years old.

Things are not hopeless though, we’ve already seen a wave of fintech and SaaS founders building new tools which will free up time and resources for finance teams to focus on strategic decision making. The first wave of tools for the finance team mainly solved for Payroll (usually the #1 cost center finance teams have to deal with), with companies such as Workday, Payfit, as well as Remote or Oyster HR.

We believe there is an opportunity for a second wave of tools to a) build integration platforms that bring data from reporting systems, operational systems, and banks to create a central view for the finance team and b) build specialised software to handle vertical workflows.

In this piece, we’ll touch on:

- What the finance team does and its importance

- The key workflows and pain points of the finance team

- The unbundling of the age-old finance team stack to build new solutions

- Where we perceive the largest opportunities to be

- A few patterns of success we’re seeing emerge in the space

What does the finance team do and why is it so important?

Finance teams build and maintain a holistic view of the company’s financial health. The CFO and their team keep track of past financial numbers (control function), map how things might develop (financial planning) and make sure the organisation allocates resources properly (financing and cash management).

The CFO and their team are in the middle of critical data flows which give them a high-level view of the organisation. As a result, the finance team can have a tremendous top & bottom-line impact. For instance, the FP&A process is a powerful tool to identify the main growth levers in a business and can drive strategy forward. By simply doing AP & AR well, the finance team can lower capital requirements and reduce potential dilution.

What are the key problems of the finance team?

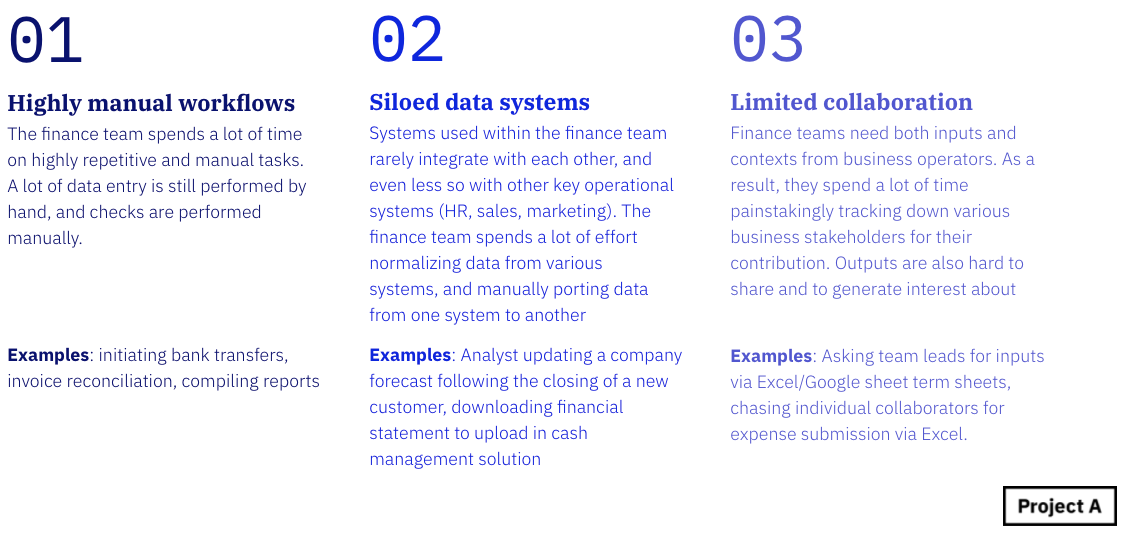

While the value of the finance team lies in their high-level strategic contributions, they often spend most of their time stitching together data from fractured data systems or running after budget holders. We’ve found three common problems which affect most of the activities undertaken by the finance teams:

The solution: unbundling existing tools to build the modern finance stack

The problems facing the finance team do not come from a shortage of trained professionals, but from limitations of the current stack. The CFOs we spoke to perceive their most urgent need to be a) tools “bundling” many different financial sources such as banks, payroll, accountancy etc., into a central view and b) vertical solutions for key workflows sitting on top of this integration layer. However, most of them seemed to believe that the only way to get there was through an enterprise-grade ERP system. They felt that the price tag (in the mid 6 figures) was too high to justify the transition.

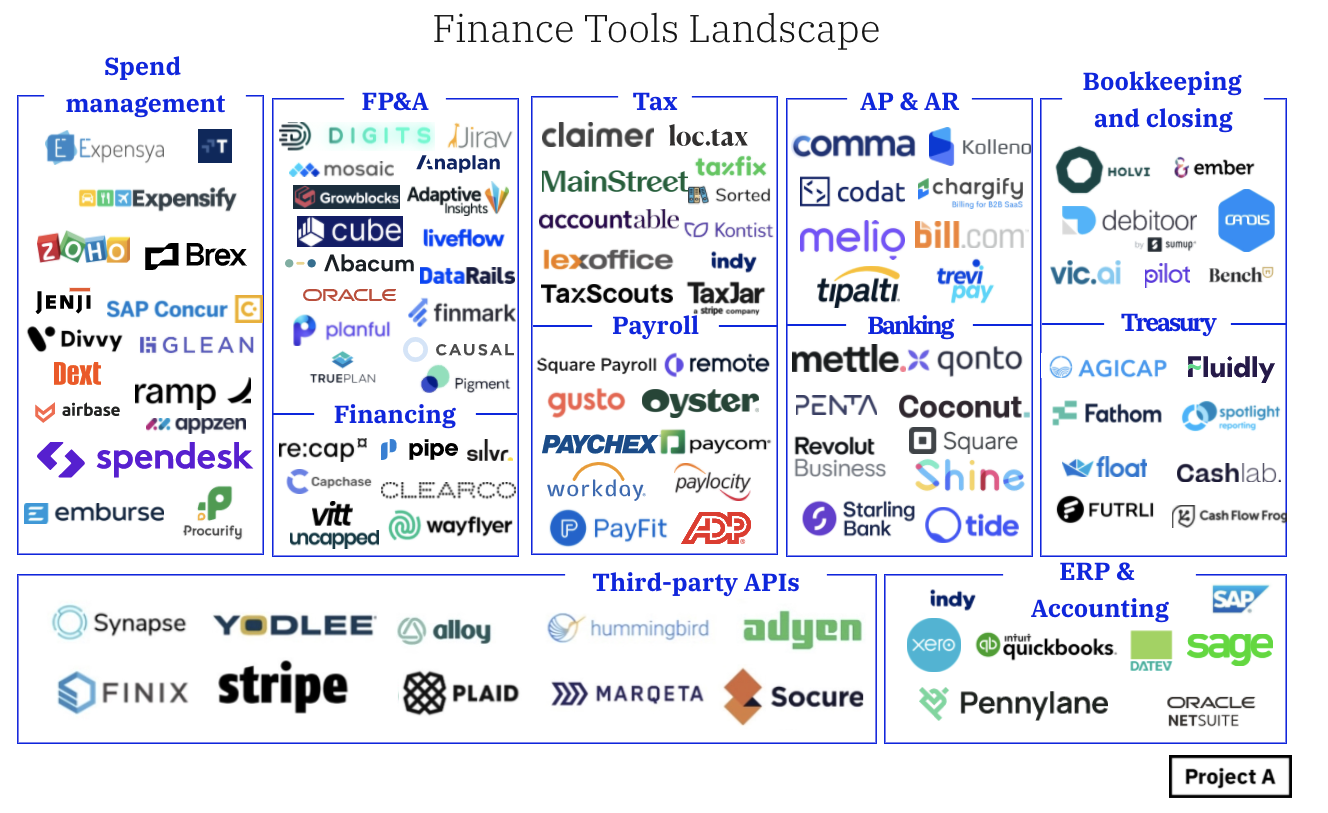

It turns out we’re seeing a new generation of tools emerging to address those issues, which we’ve mapped, splitting them by sub-sectors/responsibilities areas within the finance team:

Where are the main opportunities?

Talking to CFOs within Project A’s portfolio, we found 4 distinct areas in which we are actively looking for solutions because we believe pain point acuity and market size intersect in a way that will create billion-dollar outcomes in the next few years:

Payment automation: B2B payments are utterly broken. The infrastructure lags years behind the B2C payment stack in terms of digitisation, despite the market being 5x larger. The workflows are vastly manual (pre-approve transactions, send them in a bundle to the bank, then re-approve all of them individually before payment). We’ve identified four key bottlenecks:

- B2B checkout: Companies have numerous and complex payment options (credit card, bank transfers, invoices with specific payment terms). Merchants typically need to perform credit checks on the buyer, while optimizing for conversion.

- Managing AP/AR: The use of invoices with payment terms create massive overhead for finance teams, as they typically require invoice matching, reconciliation, and chasing late payers. On the account receivable side, we’ve seen companies like Kolleno, building platforms to manage outstanding invoices and automate their collection. For payments, we’re seeing companies such as Nook or Comma building tools to bring automation to the payment process, or Invopop, enabling developers to automate invoicing.

- Industry/geography specific transactions: In addition to the complexity layer we described, the variety of B2B payments is so great that there are needs for vertical solutions tackling specific use cases. Our portfolio company WorldRemit for instance specialises in cross-border payments and has built a B2B offering for that specific use case. Other examples of verticalised solutions would be Juni, working only on payments related to paid marketing, or Compa working on payments in the construction industry.

- Payroll: Payroll has been one of the first areas of focus for B2B fintech. However, we still see an opportunity to build companies that productize payroll altogether (rather than simply offering it as a service like Oyster or Remote). Some examples of this include Symmetrical, which are building payroll rails to automate the process, or CheckHQ.

Better FP&A: Financial Planning & Analysis (FP&A) is the process of using financial information to make forward-looking recommendations. FP&A workflows rely on highly manual and error-prone tasks conducted within spreadsheets (Excel, Google sheets), such as manually porting data from one system to another, formatting & distributing spreadsheets, chasing and incorporating late submissions, formatting reports, etc.

The main problem we’ve identified is that reporting systems and planning systems don’t speak to one another. Hence, we see an opportunity to bring various systems to streamline processes. Abacum, for instance, is building notebooks for FP&A which make it effortless to write narrative-driven pieces to analyse data automatically pulled from the accounting and ERP systems. Pigment, a Paris-based company is building a solution that makes it very easy to visualise data for analysis and projection purposes. Other companies, like Causal have built new ways to model data and to share the conclusions with the wider team. Other notable projects include Growblocks and Liveflow.

Tax & closing process: Tax and closing are cyclical processes where there is an opportunity to bring automation. Filing taxes is cumbersome and error-prone, often necessitating an accountant and managing the process with a complicated DIY system of spreadsheets. It leaves managers in the dark with regard to financial planning and how much they need to set aside for a given tax period.

The next-generation tools will retrieve data from operational systems (ERP, accounting, invoice & billing) and integrate them to automate the process. Claimer for instance has fully automated R&D claim processes. There are other interesting companies for corporate tax filing (Taxdoo, Fonoa, Hellotax, LoVAT), as well as collaboration tools around those specific workflows (loc.tax). Accountable is building tax solutions for the self-employed.

Treasury management: Most SMBs have no visibility on their treasury, and that’s often a cause of death. Most companies use DIY workflows and tools to manage their working capital, creating fragile systems which cash forecasts they can’t trust. The CFOs we spoke with also pointed out that they believed a horizontal tool would not work given the peculiarities of their business model (e.g. it’s not the same to do cash forecast for a SaaS company and a real-estate startup).

PSD2 and open banking have opened an opportunity to build tools that give SMBs a good sense of where they stand regarding working capital. We see multiple angles of attacks: spend management (Spendesk ), corporate cards (Ramp, Pleo, Brex), or scenario planning and automation (Agicap). Our conversations also hinted that cash and treasury management might require tools built vertically rather than horizontally i.e. tailored to specific business models/industries (Graneet for the construction industry, Toast for restaurants).

We also believe financing to be an important pain point for SMEs, because financing options are dilutive and extremely time-consuming. As a response, we believe non-dilutive financing to be a great entry point in the modern finance stack. Re:cap, for instance, are offering SMBs to transform their recurring revenue into upfront capital in just a few clicks, as opposed to the weeks/month with debt providers/VC investors. We’ve also seen Silvr, our of France, or Capchase & Pipe from the US

What does a winning hand look like? Patterns of great companies?

In a way, it looks like companies looking to innovate in that space are going after goliaths (Quickbooks/Sage/Xero, Excel). But what does it take to do so?We’ve noticed a few patterns which we believe lay good foundations to build a venture scale business in the space. There are obviously many more ways to do so, with approaches we could not imagine (or we’d have done it 😉). Our perception is that some approaches can give new entrants an edge and possibly a long term competitive advantage.

To wrap this up, we see a massive opportunity to serve the finance team, while creating multi-billion dollar outcomes in a largely unpenetrated market dominated by legacy incumbents or even more legacy local alternatives. CFOs have a tremendous impact on strategic decisions made by companies, and we want to invest in tools that will give them even more leverage. If you’re building in the space (and want to be added to the map!), please get in touch!