By Orphée De Bouard Sarrabezolles

It’s been a bit more than a month since I left Milan, and I think it’s now time to step back and reflect on this amazing 3-month experience. When I decided to move to Italy after graduating, I thought I would mainly be eating great food, learning the beautiful Italian language and living la dolce vita. That was until I met Anton, Partner @Project A and embarked on a 3-month journey to get to know the Italian tech ecosystem and build connections there.

Disclaimer: this article doesn’t intend to provide readers with a comprehensive overview of the state of the Italian tech ecosystem. It is merely a quick summary of my experience there, reading articles, doing research, and meeting and exchanging with the ecosystem’s key players.

Introduction

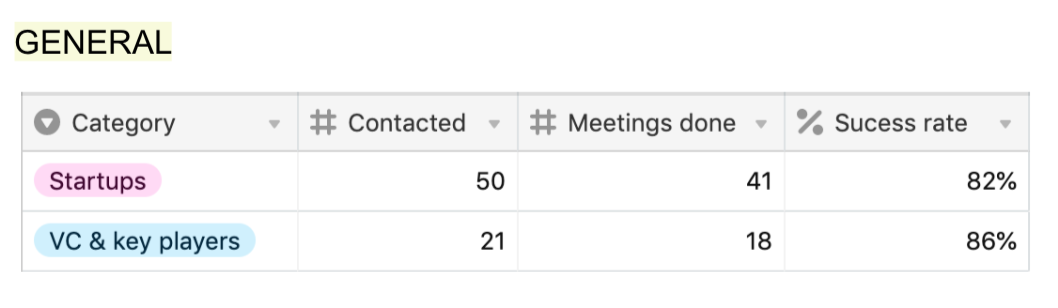

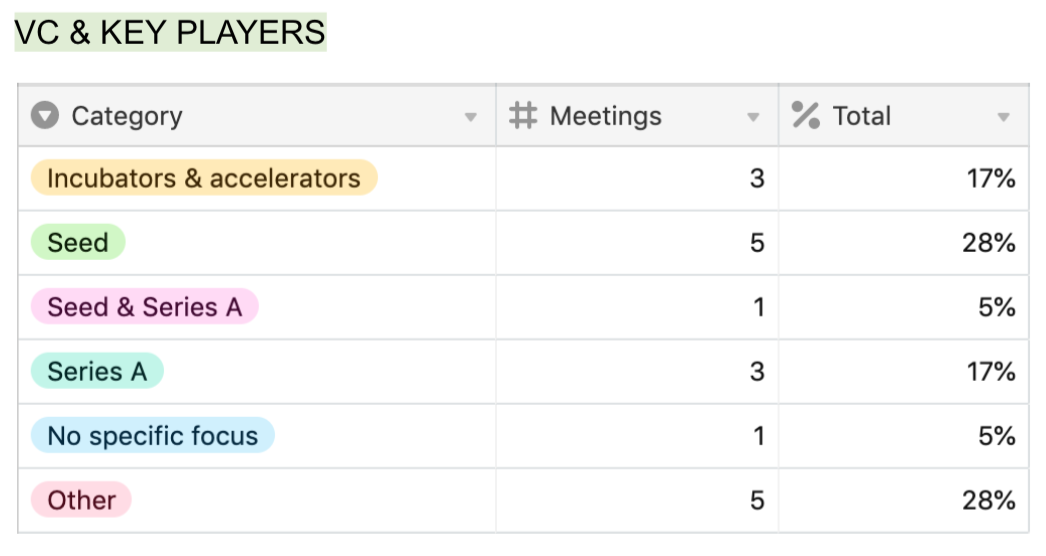

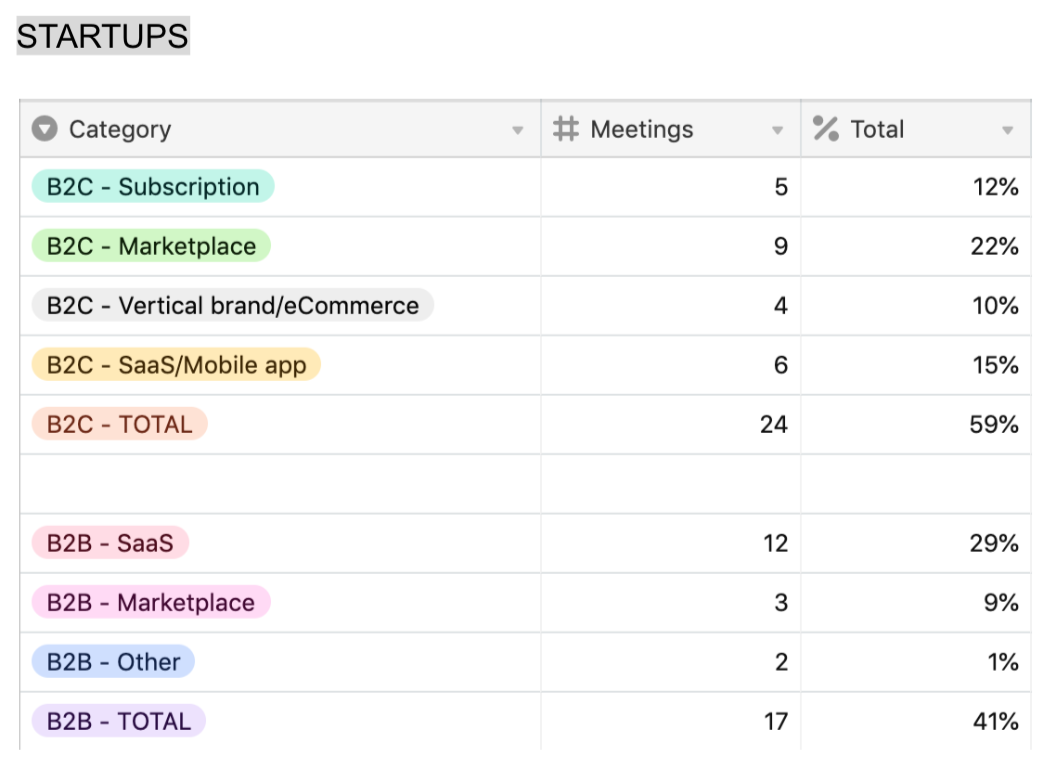

The primary goal of my 3-month collaboration with Project A was both to understand the Italian tech ecosystem’s dynamics and to build connections there. For those of you that are into statistics, here is a quick snapshot of who I met.

Before diving into the proper analysis I would like to give you some context, though. In terms of economy, Italy is ranked #4 in Europe thanks to its manufacturing, infrastructure, agriculture, science & technology, and tourism sectors. Its economy seems to be mostly driven by SMEs, while its tech ecosystem is often ranked #10 only— with Milan as the spearhead.

This is the first thing that struck me and it pushed me to learn more to understand why there was such a discrepancy. Regarding demographics, Italy has 60M inhabitants: 35% of them are over 55 years old, 70% are urban, and 33% live in the South.

Despite being a big European market, it’s a very inhomogeneous market in terms of purchasing power mainly because of a strong North-South divide, which has a lot of consequences for its tech ecosystem’s potential.

Last but not least, Italy is a country with a tradition of innovation, historically supported by industries like automotive and fashion, but that has long been experiencing slow digitalization. The latter seems to be largely due to bureaucracy, stringent regulations of all kinds, change resistance and some other deeply-rooted cultural features.

🏛️ Institutional environment

From a generic perspective, the country suffers from bureaucracy, red tape, a certain tax burden, and complex laws and regulations. Although Italy introduced the Italian Startup Act in 2012, which made it simpler to register a new company, relaxed labor regulations, introduced tax incentives for investors and created a fast-track startup visa for entrepreneurs, the country is still ranked 79th out of 180 countries for “economic freedom” according to the Heritage Foundation’s 2017 index.

Traditional industries are still seen as paramount to Italy’s economic success. It is also taking time for Italians to build up the confidence to purchase products and services online as there is a general lack of digital education. On another note, the high savings rate perfectly illustrates the risk avoidance mentality that still seems to prevail and unfortunately, savings are not yet poured into VC for the aforementioned reasons. From my understanding, a lot of family businesses tend to choose less risky assets over VC.

Finally, the big economic differences between the North and the South are a huge institutional brake on scalability, as already mentioned in the introduction.

Nevertheless, the Italian government has been fostering the innovation sector and has been willing to put a lot of money into VCs recently: with the government’s backing, the National Innovation Fund aims to raise millions of euros of venture capital for small and medium enterprises within three years and there should be other incentives, including generous tax relief, that will take the total to 2B€. This is definitely key to creating the right conditions for the Italian ecosystem to take-off and could prevent many Italian entrepreneurs from deciding to go abroad to launch their business.

In that regard, the path between Italy and the UK is a pretty well-trodden one (estimated 100,000 Italians living in London) and a number of well-known UK startups have been founded by Italians, such as King co-founded by Riccardo Zacconi, Depop that started in Italy and later moved to London, and a brace of up-and-coming FinTech companies — Soldo, Yapily, Truelayer.

💵 Investments

Following the Internet bubble, nothing really happened between 2003 and 2012 in Italy. 2012 seems to be a turning point and the country now has a few renown VCs: P101, 360 Capital, Team Innogest, Indaco, United Ventures, PrimoMiglio, LVenture (with LUISS ENLABS), Italian Angels for Growth, etc. Pre-Seed, Seed & Series A stages are pretty well-covered now but Series B+ stage VCs are quite hard to find as for other European countries actually.

On a side note, the current typical rounds in Italy are the following: Seed 200K-1M€, Series A 1M-5M€, Series B & later stages 5M€+. Companies like Brumbrum (that has raised a total of 30M€ with United Ventures and Accel so far) and Project A’s portfolio company Casavo (raised 60M€ within 2 years of operating) are exceptions.

The Italian startups’ financing journey is also less linear than what one is used to in France, Germany or the UK: sometimes there are multiple Seed and Equity crowdfunding rounds because of a lack of capital. As a general evolution, there is more and more Italian deal flow coming in and a couple of EU funds start to look at Italy.

While Italian VCs seem to find most deals through inbound, a proper culture of scouting/sourcing starts to spread. In addition to early-stage VCs, the Italian tech scene benefits from the presence of incubators/accelerators like LUISS ENLABS, Digital Magics, AlmaCube, or PoliHub, that are trying to provide very structured programs (YC’s influence) for startups. All in all, VC investments are a pretty recent thing in Italy and the ecosystem is said to be aiming to reach 1B€ of VC investment in 2019 — compared to 500M€ in 2018.

💻 Tech environment

Every aspiring tech ecosystem needs a hub and Milan has all the ingredients to be a hub: capital from private savings, VC funds, infrastructure, universities, quality of life, open-minded people, etc. There still seems to be a long way to catch up with Europe’s main hubs Paris, London, and Berlin, though.

Indeed, Europe’s biggest startup hubs are also growing the fastest. Apart from Milan, Turin seeks to become a hub and a new initiative has just been launched: OGR Torino (in partnership with Techstars) has the goal of bringing 500M€ into Turin’s ecosystem and accelerating 1 000 startups in the next 15–20 years.

Regarding talent, tens of thousands of young Italians emigrate overseas each year in a search for better opportunities, and many of them are highly educated. The result is that Italy’s technology sector struggles to fill thousands of skilled jobs, despite the county’s high unemployment rate, due to a shortage of talent. However, the developer pool is getting bigger and bigger and Italy now counts more than 314 000 professional developers — ranked #7 in Europe.

Looking at schools and universities, we can notice a lack of entrepreneurship-focus streams of studies, as traditional industries are still prioritized. Therefore, more and more digital schools emerge like PI School, Talent Garden, or a couple of bootcamps, to fill the gap. Some universities have good incubators but the latter are often more focused on turning research projects into entrepreneurial projects.

Lastly, there isn’t any major Italian tech event. Only local ones that strive to gather all key players (Corporates, VCs, startups, digital schools, etc).

🚀 Startups

It feels like when an ecosystem is not yet mature enough, there are more opportunities on the consumer side and it seems to be the case in Italy. Even though there are fewer business software opportunities than in other markets, B2B still has to be looked at, especially given the number of SMBs in the country.

In terms of verticals, the current trendy topics are tech applied to the traditional Italian economy like FashionTech, consumer companies in general like eCommerce, TravelTech, digital health, InsurTech/FinTech, and some interesting stuff in B2B around Big Data.

Moreover, Italy seems to have an edge on BioTech/MedTech (many startups founded, key players like Team Innogest

) as well as on SpaceTech. Based on the insights I’ve been able to gather from Italian VCs, the lack of entrepreneurial culture is getting compensated and Italian entrepreneurs are more and more interested in models and industries scalable beyond the Italian market.

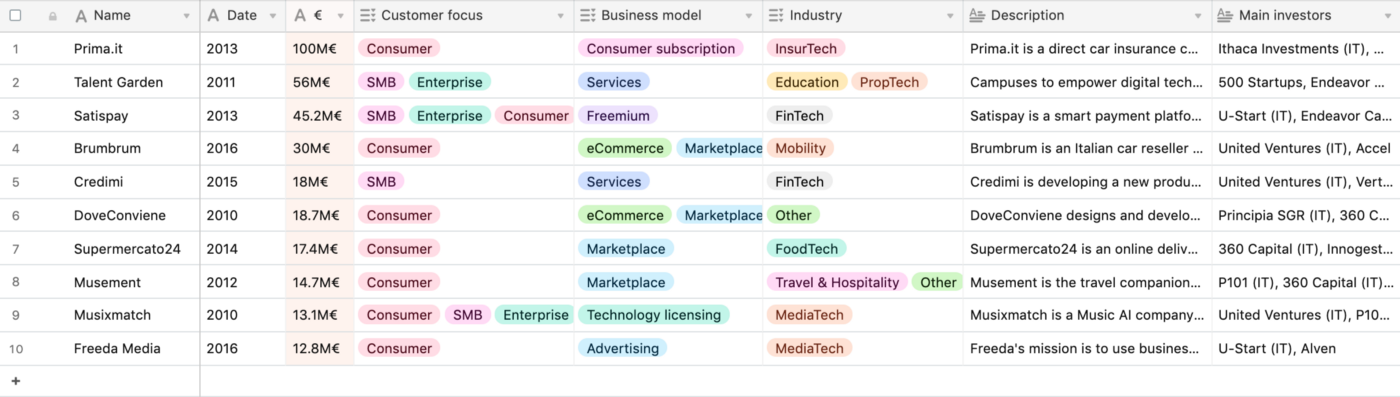

Italy has a couple of well-funded startups, and you’ll find another screenshot to illustrate that below (UPDATE: Casavo is now part of it with its 50M€ Series B, and Freeda Media raised another 14.5M€).

🚪Exits

From a general perspective, there are many SMEs in Italy with insufficient financial power to acquire startups. As for most European countries, the country also suffers from a lack of big tech companies able to do strategic acquisitions conversely to what happens in the US.

There is not a single Italian unicorn and there are very few notable exits. As a consequence, not a lot of money is being recycled into the ecosystem: this virtuous circle is usually a key ingredient to having an ecosystem take off.

Two main points have to be raised: most Italian exits are either BioTech/MedTech-related or small acquisitions around 1M€ of startups in their early days (2–4 years of existence). Musement (bought by TUI Group in Sept. 2018) is probably one of the biggest acquisitions. It was funded by P101 and 360 Capital among others. Other notable exits include Facile.it (bought by EQT in May 2018), Jobrapido (acquired by DMGT in April 2012), and Pizzabo (bought by Rocket Internet in February 2015 for $55M).

🔚 Conclusion

Italy seems to have gathered a lot of ingredients: pre-Seed/Seed players, bigger early-stage VC funds, a hub in Milan, more and more public investments into the ecosystem, first success stories, universities/research more bounded to the entrepreneurial world, new digital schools and bootcamps…and it will hopefully take-off within two years.

The Italian ecosystem will probably have a hard time becoming part of the top 5 European tech ecosystems though, with the two following elements being key: traditions/Italian specificities like economic differences between North and South, lack of digital education, prevalence of traditional sectors and players, and the lack of big success stories/exits, which is paramount to an ecosystem’s ability to recycle money and trigger a virtuous circle on its own.

Nevertheless, we see some movement with the first success stories like BrumBrum & Casavo drawing international attention, which will help the ecosystem gain relevance. Furthermore, Italy could actually go back to its fundamentals like aerospace, precision manufacturing, FoodTech, AgTech, and Tourism…to better compete with other ecosystems.

On a personal note, I really enjoyed discovering a whole new ecosystem from scratch and I would like to thank every single person that I’ve met there as I’ve always been well-received! And of course a big thanks to Project A, you guys rock!

I’m now off to a new challenge at henQ where I’ll be looking for early-stage B2B software European startups.