By Enrico Mellis and Sharanya Eswaran

The last time the eyes of everyone in the world were fixated on FedEx was in 2000, when Tom Hanks starred in international blockbuster ‘Cast Away’. Today, billions are watching closely as FedEx ships the first vaccines from Pfizer’s facilities in Kalamazoo.

When will the vaccine get here? How fast can we get out of this mess?

Around the globe, excitement peaked when Pfizer and BioNTech published vaccine results (causing a historic public markets frenzy, best summarised in this meme). Margaret Keenan became the first person in the western world to be given a Covid-19 vaccine. In the UK, this injection kicks off a first-run of “800,000 doses of the Pfizer/BioNTech vaccines” . As I’m writing this, other countries are following.

The vaccination of the global population will be the “largest product launch in the history of humankind”.

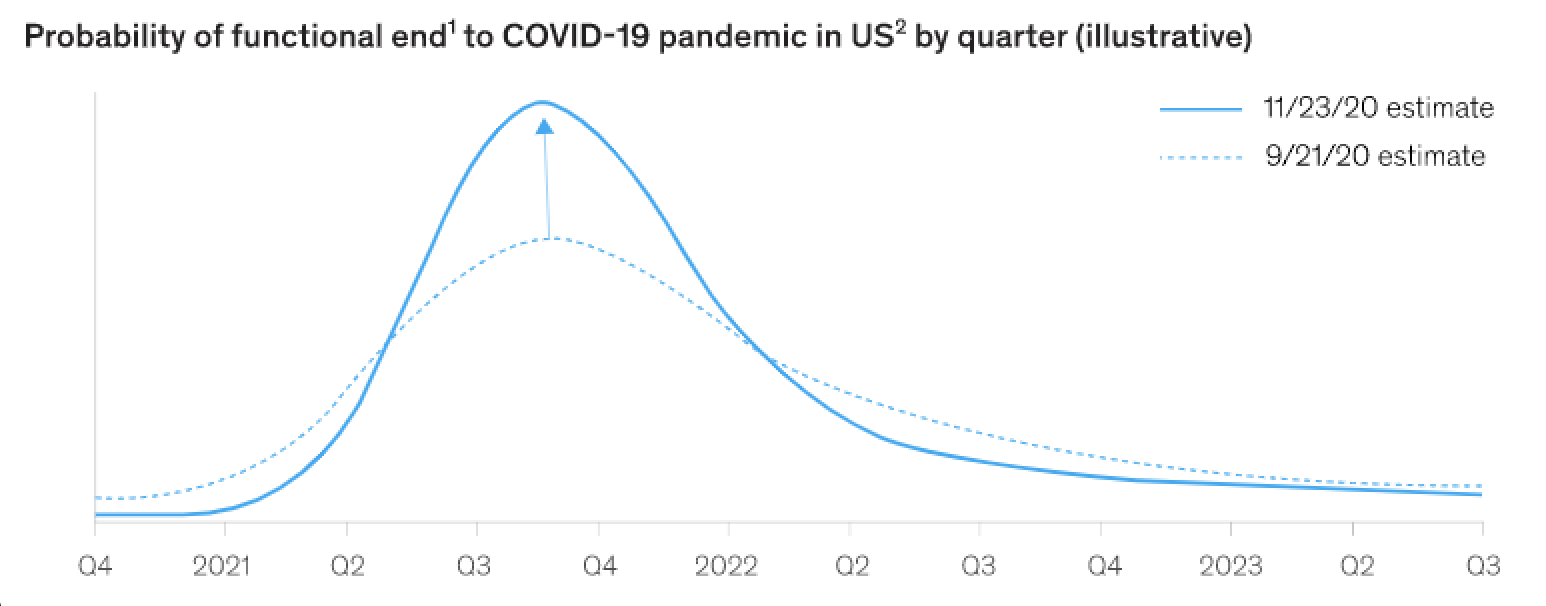

The pandemic’s timeline depends on it. Studies show that the most likely timeline reaches the functional end of the pandemic in Q3/Q4 2021. One of the main drivers behind this timeline are the high expectations around distribution.

However, supply chain issues could massively slow down the timeline to Q3 2023.

Vaccines don’t save lives, vaccination does

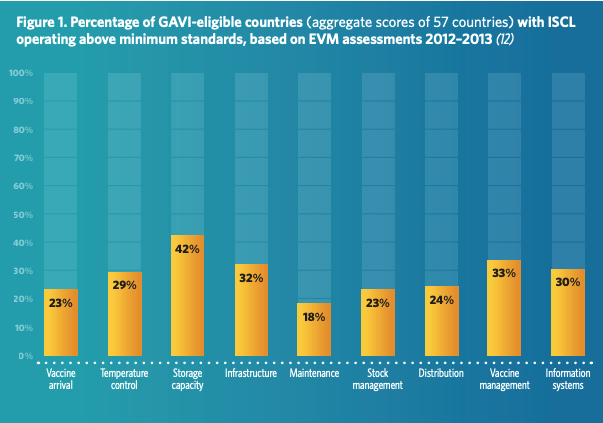

Shippers, carriers, governments and manufacturers have been preparing for months to make the impossible possible. Looking at where the world’s countries currently stand in terms of the readiness of their Immunization Supply Chain Logistics (ISCL), the numbers don’t look as promising:

The logistical complexity is unparalleled — a current estimate says 60% of the world’s population will need a vaccine. Pfizer/BioNTech are aiming for 25m doses by EOY 2020 and 630m in 2021. It will take other players like AstraZeneca, Moderna, Merck, etc. to satisfy global demand. The US alone have purchased 700m doses from various companies in advance — their deal with Pfizer alone costing $1.95bn for 100m doses (Source).

After production comes packaging, shipment and administration. The orchestration of that requires not only shipping a vaccine, but also swabs, masks, gloves, syringes, etc. The vaccine is a double-dose vaccine, so factor in all materials at least x2. 850m syringes are estimated to be needed in the US alone. And at the same time, you need the personnel to administer the vaccine — personnel who need to be vaccinated. How many staff need to be vaccinated depends on the number of vaccines a given region receives — which in many countries, is unclear. Puerto Rico already experienced the first bigger public hiccup — they received only half the vaccines they were promised.

Due to their volumes, additional supplies will be shipped by sea and road freight. That will take longer — up to 4 months — than the 3 days needed for vaccines to be air-shipped. Furthermore, air cargo capacities are insufficient. All global air cargo worldwide is moved by around 2,000 air freighters and 22,000 regular jetliners. The IATA (International Air Transport Association) estimates that 8,000 747s would be required to deliver a single dose to the world’s population.

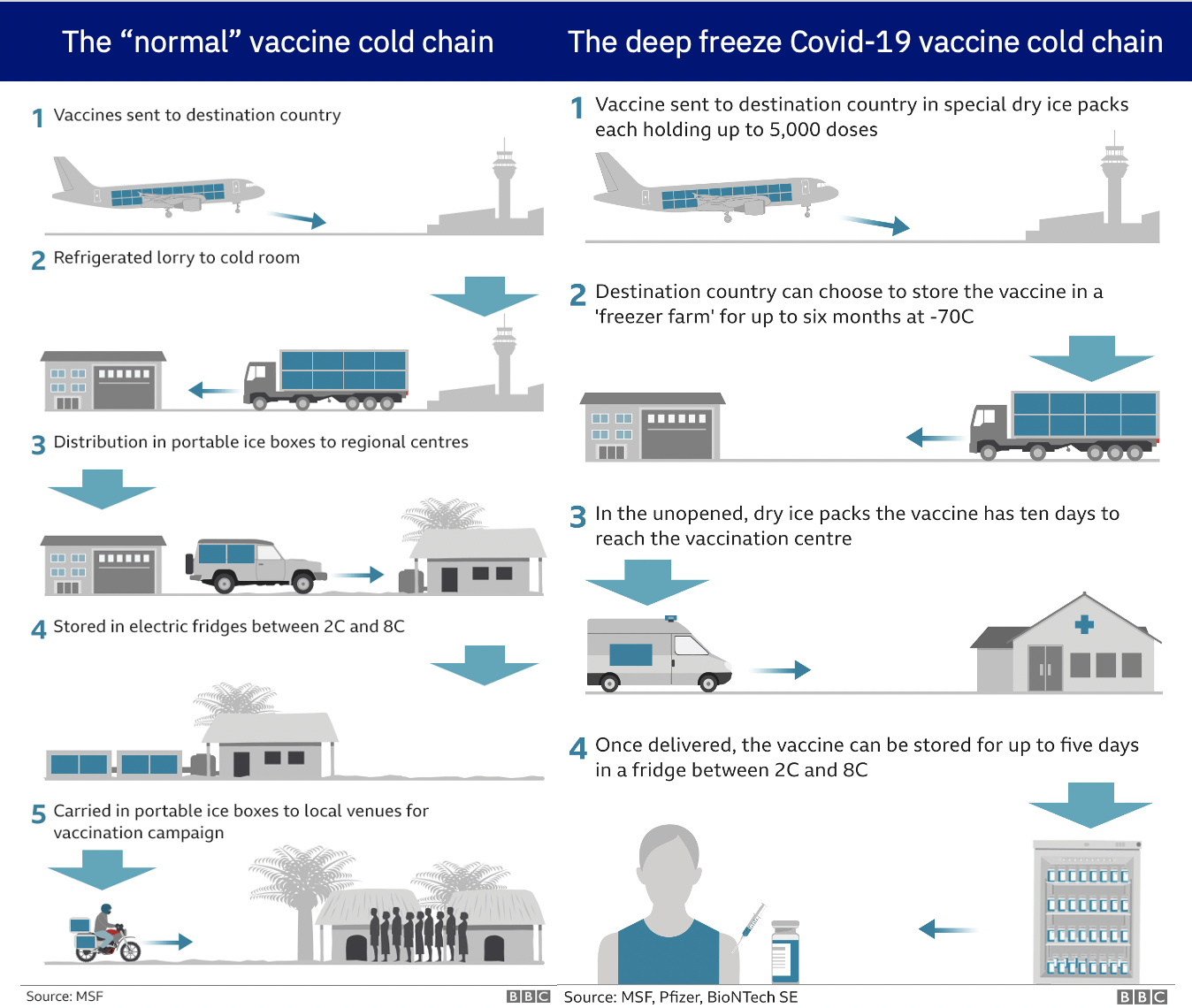

The cold chain (which doesn’t exist yet)

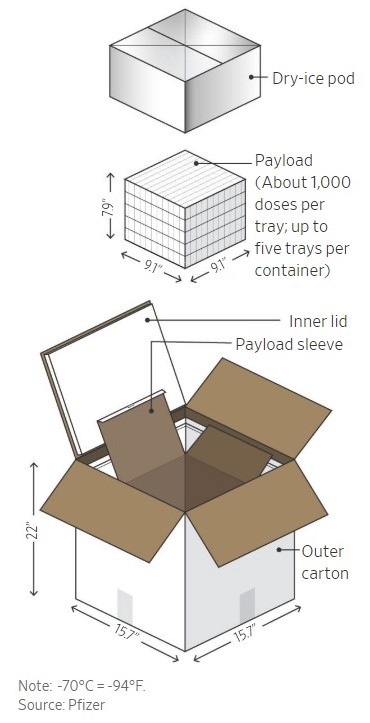

How do you source millions of specifically-designed boxes which maintain an internal temperature of the North Pole (-70 °C for the BioNTech vaccine, 2–8 °C for the one from Moderna) and distribute them across the globe without disrupting the cold chain?

Pfizer designed a box for the vaccines to be carried in. It holds 4,875 doses and needs a refill of 23kg of dry ice every five days — to keep the vaccine functional for 15 days.

Large logistics groups such as DHL & medium-sized pharmaceutical logistics companies are already preparing for the special transport conditions. UPS & FedEx are building freezer farms with 600 freezers each holding 48,000 doses of the vaccine. But UPS and FedEx can’t do this all over the globe. These special cooling systems are not available in most parts of the world. You can’t even get a cold can of Coke in some of these countries where the cold chain is incredibly fragile. In large regions of the planet, 25% of all fresh produce, which only has to be kept a little above 0 °C, is wasted due to breaks in the cold supply chain. The WHO estimates that, in 2011 alone, 2.8m doses of vaccines were lost because the cold chain was broken — in Nigeria and Ethiopia for example, almost a third of all cooling facilities are non-functional in the first place.

Hence, everybody is still waiting for the game-changing vaccine that does not need more than 0–8 °C.

And even with the functional equipment, humans make mistakes. At all points of “changes in custody” (e.g. from air cargo to the truck), the risk is high for mistakes to happen. Refilling the boxes is tricky. Pfizer recommends the boxes are not opened more than twice a day, and should be closed within one minute, even when refilling with dry ice. It is also likely that dry ice will run out in most countries — with some producers already at their capacity maximum.

Doesn’t sound dramatic enough yet? Here come the hackers…

To make matters worse, supply chains for Covid-19 vaccines have been targeted by criminals heavily. Several government bodies have issued increased worries around various cyberattacks against vaccine shippers and carriers. From manufacturing to distribution, officials have “noticed an uptick in attacks”: “[Our] suspicion is that all parties in the cybercriminal underground from ordinary criminals to nation state representatives recognize that the vaccines represent a golden opportunity and are responding as such”. Also, officials’ private homes and cold storage groups are being targeted by a “global phishing campaign”. Cold storage companies don’t have resilient cybersecurity systems and hackers can enter their systems.

“Advanced insight into the purchase and movement of a vaccine that can impact life and the global economy is likely a high-value and high-priority nation-state target.”

BBC

Healthcare information systems under pressure

The centrally organised orchestration of vaccinations has to be as efficient as possible — the BioNTech vaccine becomes unusable 6 hours after thawing. Databases for patient data or medical supplies data are not integrated with vaccine providers and federal agencies. This in combination with the complexities of double-dose vaccination will put healthcare systems under huge pressure to overcome tiresome data policies and digitalise processes.

Staffing will be an absolute nightmare to manage. In Berlin for instance, expected capacity are 3,400 vaccinations per day and center. One challenge will be that the queues for the vaccine don’t become super-spreader events. In addition, not only must there be enough medical doctors on site, but drivers, helpers, etc. In all countries, governments will have to rely on other aid organisations, the armed forces, hospitals, and volunteers for help.

In the middle of difficulty lies opportunity

Previously, vaccination efforts have focused on individual vaccination supply chains — from measles to yellow fever, there was rarely a unified effort to build a resilient supply chain which can deal with a global pandemic. This is the first time in history that a pandemic has reached the whole world simultaneously. The requirements for supply chains have never been so high. The only consolation is that everybody is grappling with this — which is why we think it’s a great opportunity for creating better supply chains and a better healthcare system.

Project A: Our view on logistics

Project A invested early in Coureon, Intelipost and Sennder and since then we have spent quite some time diving deep into logistics & supply-chain technologies. As an emerging winner in the road freight-forwarding sector, Sennder is one of the rare cases of startups who have cracked open the hard-to-penetrate logistics market in Europe. We believe that Covid-19 will be a catalyst for startups tackling these challenges.

Logistics have always been driven by technology. Containers, pallets and larger vessels enabled scalability, bringing costs down. The resulting explosion in world trade created new challenges & complexities.

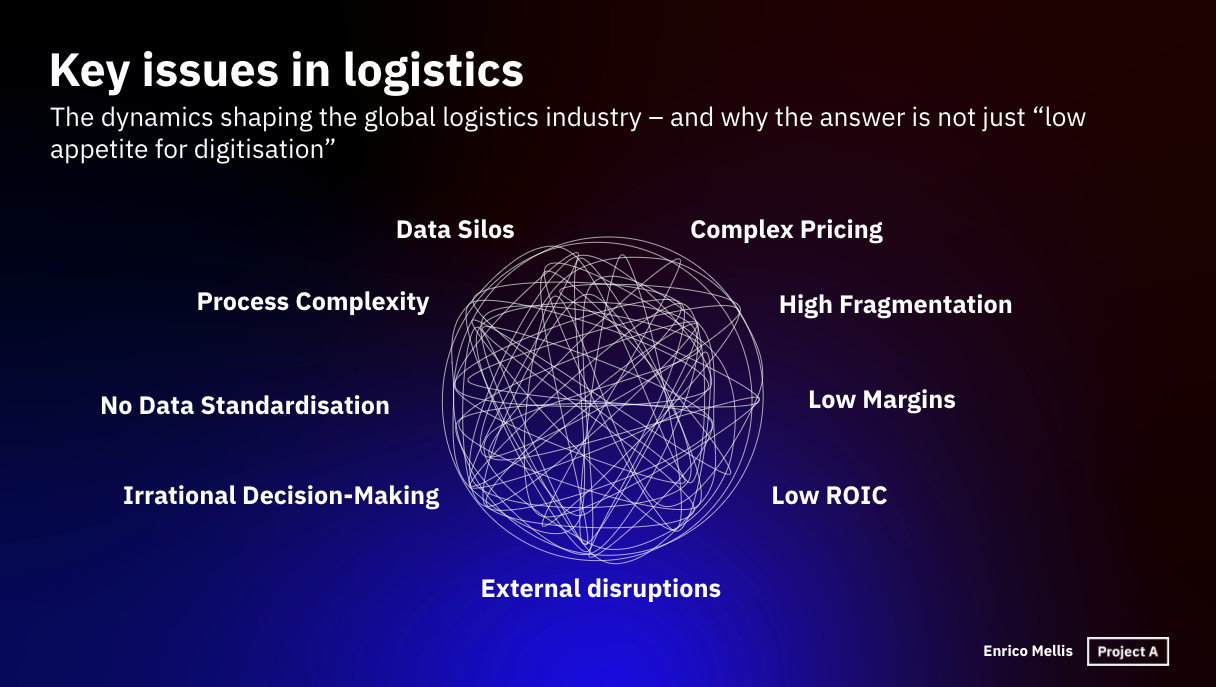

In logistics, the key issues hampering technology and innovation adoption are reinforcing one another. These are not issues of technology: we have tracking devices, cloud infrastructure and most of the other puzzle pieces needed to gain full supply-chain control. The problem is that the systems are too complex to build quick-fix solutions. This is deeply rooted in the nature of how the logistics industry has evolved and how it’s shaped by external forces. The reason the logistics space is so hard to penetrate for logistics startups is not just a “low appetite for digitisation”. The answer is a bit more messy than that:

- Process complexity — A large number of “changes in custody”, customs regulations, inspections, re-routings, fulfilment, etc. involve so many different players (see “high fragmentation”) that the sheer orchestration of a cross-border shipment is becoming an impenetrable chaos to manage.

- Complex pricing — As a result, multiple tax- and customs-policies across various changing currencies makes pricing a task in and of itself.

- No data standardisation — There are very few cases of homogenised data standards and most of communication is still based on heterogeneous data formats & languages.

- Data silos — Due to this lack of standardisation and fierce competition (see “high fragmentation”), owners of data guard it and are reluctant to share with other actors in the market.

- Irrational decision-making — Based on low levels of digitisation (e.g. see “data silos”) few software products manage to provide benefit, forcing actors to make decisions based on intuition and experience.

- High fragmentation — A wide variety of players, ranging from independent truckers to incumbents like DHL, Kühne + Nagel, etc. are trying to gain market share in a competitive fight where price often is the only differentiator and all long for economies of scale.

- Low margins — The aforementioned fragmentation, along with irrational decisions and both internal & external disruptions lead to low margins, despite the industry’s top-line growth.

- Low ROIC — Driven by low margins and (for most players) complicated growth outlooks and resulting below-market multiples, investors are skeptical about logistics and financing to grow & innovate is hard to come by.

- External disruptions — Logistics is an inherently physical industry. Natural disasters, strikes, war, and other catastrophes (pandemic, anyone?) cause countries to shut down, trade lanes to clog up and roads to freeze.

Little funding in Europe compared to the US

The total VC dollars going to logistics startups in 2019 globally was $6.3bn — of which logistics startups in Europe received a meagre 5%, compared to 35% received by their American counterparts. Yet, we see maturing cases such as Sennder or Forto as pioneers of a European logistics landscape, which will attract more investor interest and nurture more winners.

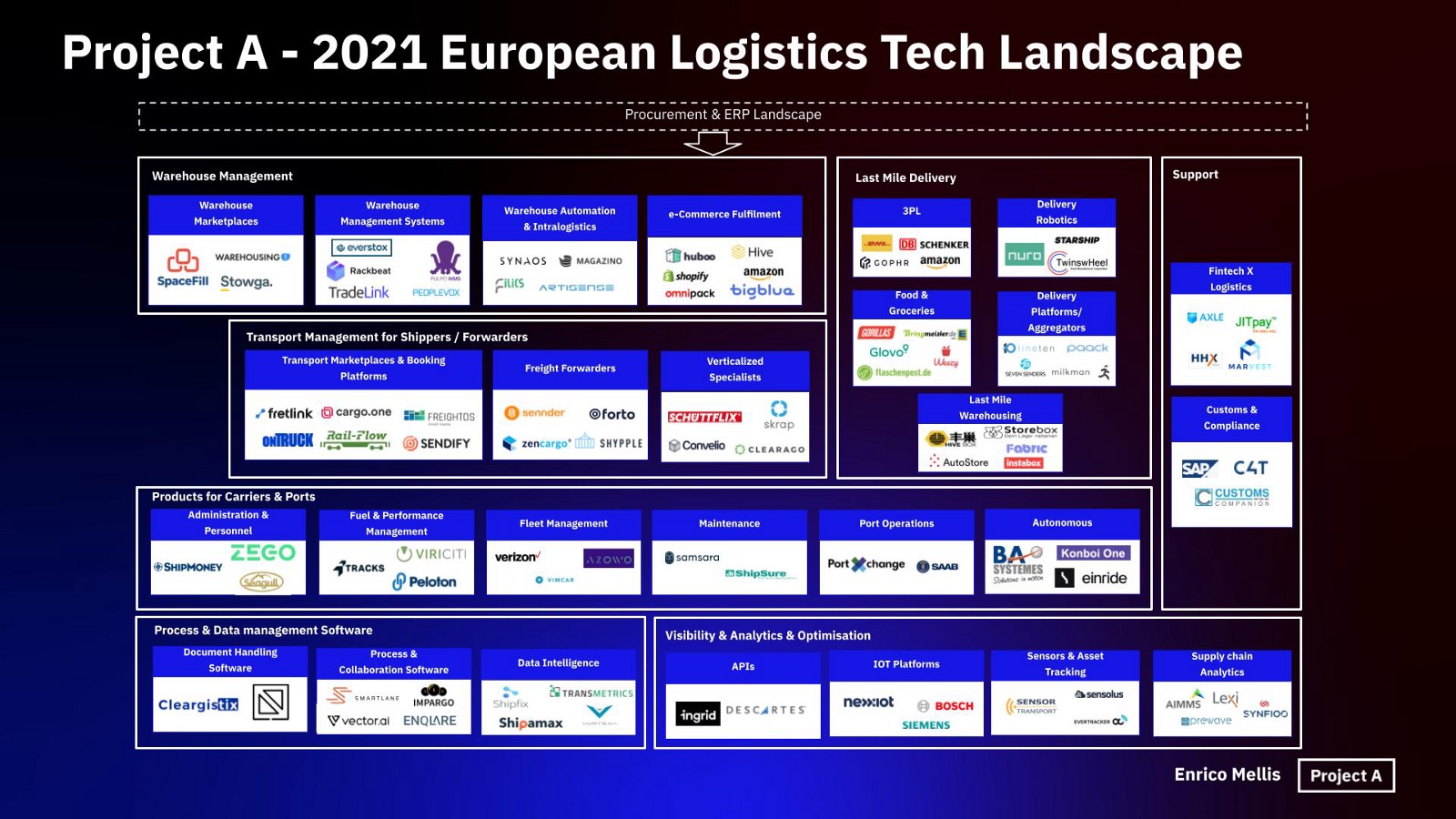

Project A — 2021 European Logistics Tech Landscape

As a first glimpse, we would like to present you with our European logistics technology landscape, highlighting the areas of logistics startups we see in the market in Europe, including some mentioned highlights and examples.

In 2021, we will publish a deeper dive into the specific hypotheses we have in logistics including which models we are most bullish about, which markets we think are most attractive and which technologies we track closely. We will give you more depth on why we believe that the verticalization of both horizontal software plays and models from more mature adjacent markets (e.g. MarketingTech or Fintech) makes sense in a gigantic market such as logistics, where we see the future of last-mile infrastructure and why the future of logistics might be in APIs & smart data extraction.

Stay tuned, stay healthy. See you in 2021!

Thank you!

Sharanya & Enrico