By Sam Cash

UberCab, a company started in 2009 and inspired, in-part, by James Bond tracking his car with his Sony Ericsson in Casino Royale, is today IPO’ing at a market capitilisation upwards of $80bn — S-1 filing available here.

Uber is the defining company of this current technological and economic cycle — characterised not only by its sheer size, its bold and unapologetic global ambitions, its search for profitability but unfortunately also for the company’s choice behaviour towards employees, driver partners and customers.

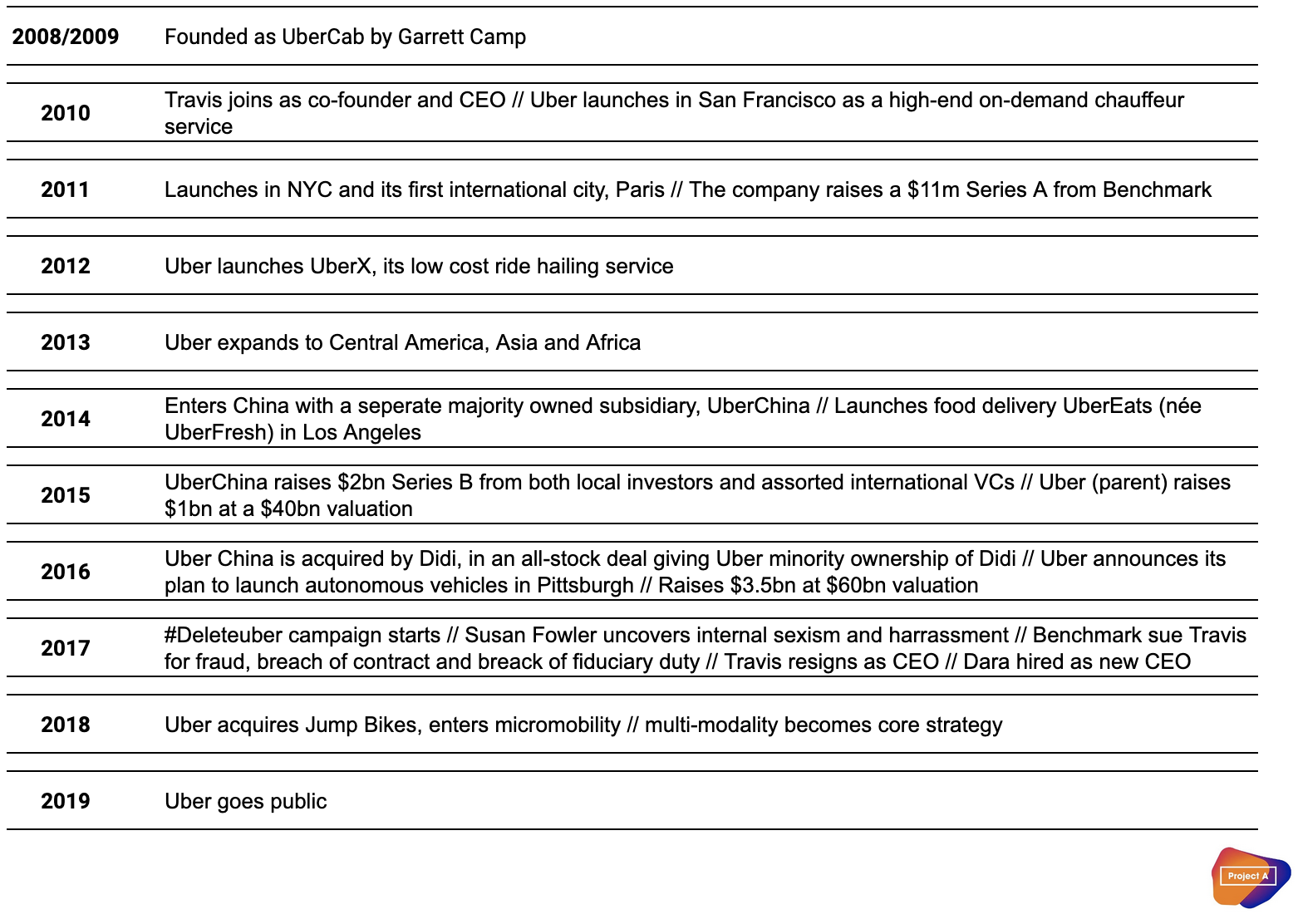

First, an abbreviated company timeline:

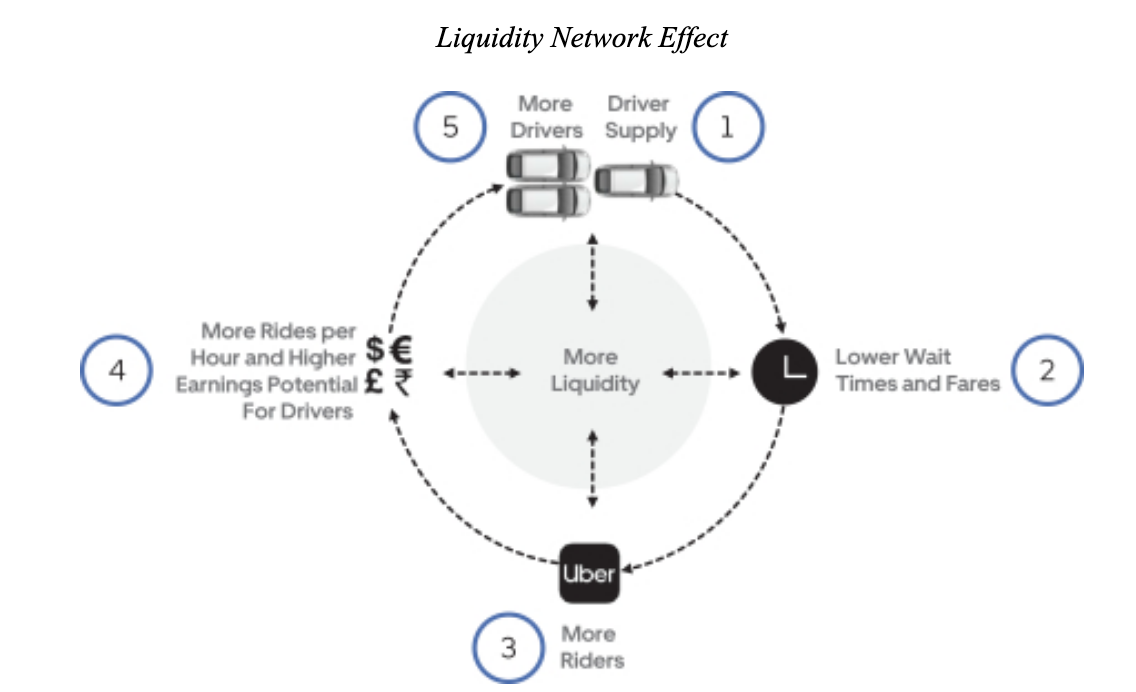

Uber’s growth to date, has been categorised as aggressive, bold, unapologetic and often blurring the lines of the moral and lead code. Much of the global growth was spearheaded by then CEO Travis Kalanick and the significant capital raised by the then SVP of Business, Emil Michael. During the heady days of this partnership, Uber argued that ride-sharing was ‘winner-takes-all’, due to needing to providing sufficient marketplace liquidity for the service to operate with sufficiently low wait times (<5mins), as per the below graph:

It’s become increasingly clear that ridesharing, at best, is winner takes most and that a highly liquid marketplace is only partially defensible. Unfortunately for Uber, the network effects are only partial as switching costs are relatively low for both supply and demand. Uber was successful in its goal of securing much of the global land grab, let’s explore which opportunities and challenges lay ahead.

IPO Filing

Firstly, a few very notable omissions from this filing:

- How much it costs Uber to acquire drivers and riders

- What is Uber’s retention rate for drivers, riders, restaurants and eats customers

- No cohort analyses (which has come to expected for tech S1s)

- Ride-sharing revenue and profitability by geography

- UberEats revenue and profitability by geography

- Seperate take rates for Ride-sharing and Uber Eats

Beyond this lack of tangible data, one of the key issues many sophisticated investors will have is how to undertake a sum-of-the-parts-analysis of Ridesharing, Eats, Freight, ATG, Jump Bikes, wholly owned affiliates (Careem) and minority owned affiliates (Didi, Grab, Yandex.Taxi). Unfortunately, this opacity will be unlikely to dissuade retail investors, many of whom assume Uber to be a wildly successful company, however you define that.

Growth at all costs

Uber has raised over $17bn, in primary and debt funding to date. Whilst, the company has been active in releasing quarterly numbers in the last year or so, much of what lies under the hood remains blackbox to those other than the largest shareholders.

One important narrative that is non-obvious looking through the company’s timeline or S1 filing is around autonomy. Whilst the company raised mind boggling sums of money, their search for positive unit economics were largely explained away by scale and by the possibility of replacing the largest element of COGS, the driver, with fully autonomous vehicles (more on autonomy later).

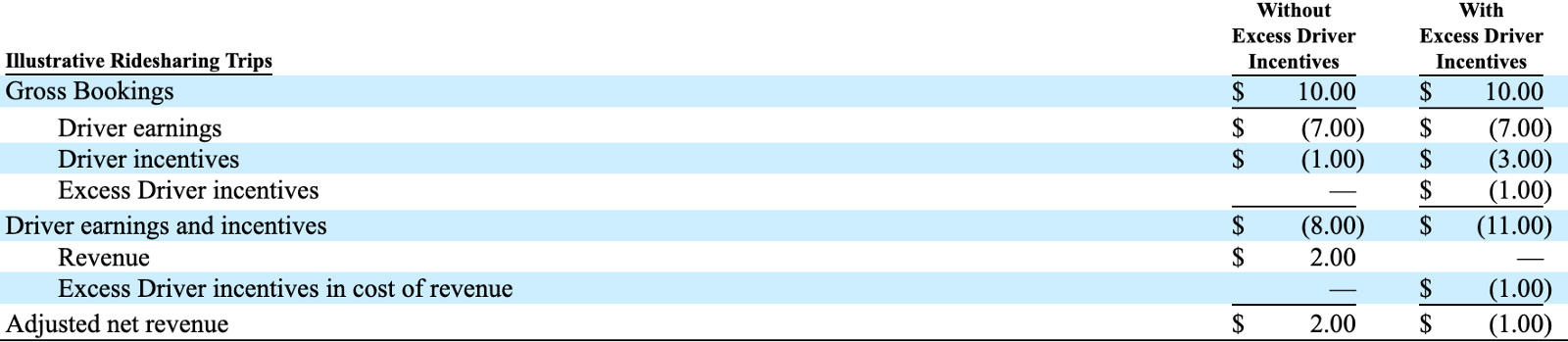

Subsidies — whilst the subsidy wars seems like a distant memory (Reminder: Uber spent billions effectively subsidising liquidity on both sides of the marketplace (drivers+riders) in order to build a moat around their marketplace). This effectively meant that riders enjoyed lower prices, whilst drivers had a higher take rate for their rides. Typically, Uber provided subsidies for 12 to 18 months after entering a new city, subsequently imposing price increases thereafter. This change in unit economics is well illustrated by Uber:

Whilst the land-grab induced subsidies have cooled off, the S1’s narrative reads much like an early to mid-stage company, where the company upside is painted through a long-term vision and upside lies in continuing to penetrate a large market. Arguably, the company is uniquely poised to do so with a platform that not only dominates mindshare, but also boasts 91 million customers and operations in 63 countries:

“We believe that Personal Mobility represents a vast, rapidly growing, and underpenetrated market opportunity. We operate our Personal Mobility offering in 63 countries with an aggregate population of 4.1 billion people. Through our Personal Mobility offering, we estimate that our platform served 2% of the population in these countries based on MAPCs in the quarter ended December 31, 2018”

— Uber S1

Platform, products and profitability

Uber as a company has ingrained multi-product DNA, it’s easy to forget that the company has moved from luxury chauffeur driven cars to ride-sharing to Eats and now, entirely new adjacent products such as route finding and multi-modality. Let’s take a deeper look into the three core products;

Ridesharing — the core product(s), ranging from Pool to UberX to Lux, is the beachhead the company has built its business around and launched multiple products off of.

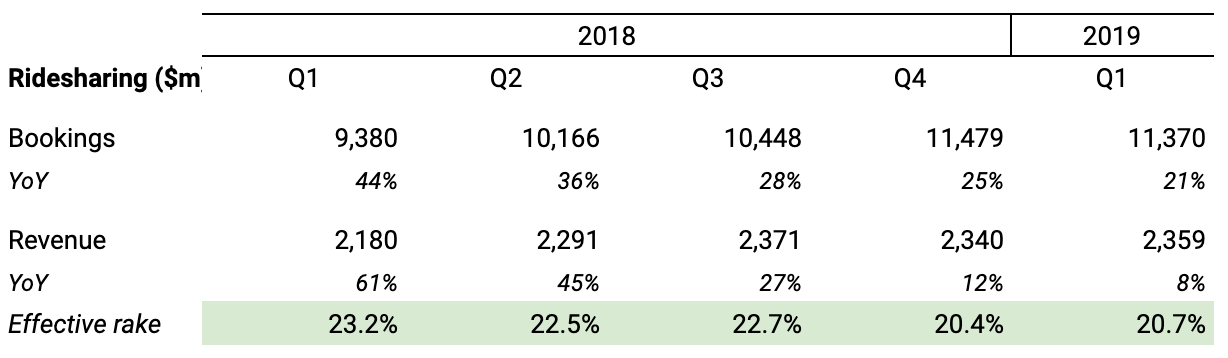

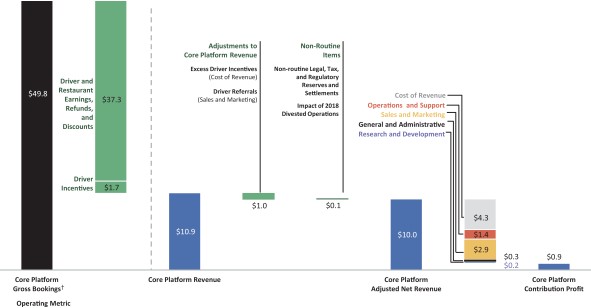

Ridesharing year-over-year growth is decelerating, whilst from Q4’18 to Q1’19 gross bookings actually contracted, though adjustments to take rate actually yielded a modest increase in revenues over the same period. There are two main questions here; growth and positive unit economics!? Whilst, the S1 is sparse in terms of information, we understand that on a unit basis there is underlying profitability and some scalability to their fixed cost base:

In the last few years, Uber has brought increased price opacity to riders and drivers alike, through upfront pricing and penalties for drivers. This has allowed them to modulate pricing on both sides of the marketplace, though much to the dismay of driver partners.

Eats — or food delivery more specifically, is a natural product extension to operating a large transportation platform. The product connects consumers with restaurants, and provides delivery of menu items.

The importance of Eats is a few-fold. Firstly, theoretically providing Eats to existing drivers increases their utility, as they can fill dead legs with Eats orders. The product also increases the number of both drivers and consumers on the platform, who can later be cross-sold different products. Less appreciated, is that Uber have consistently used UberEats as a strategic stalking horse in cities where ride sharing operations are banned, in order to generate a groundswell of support and maintain mindshare.

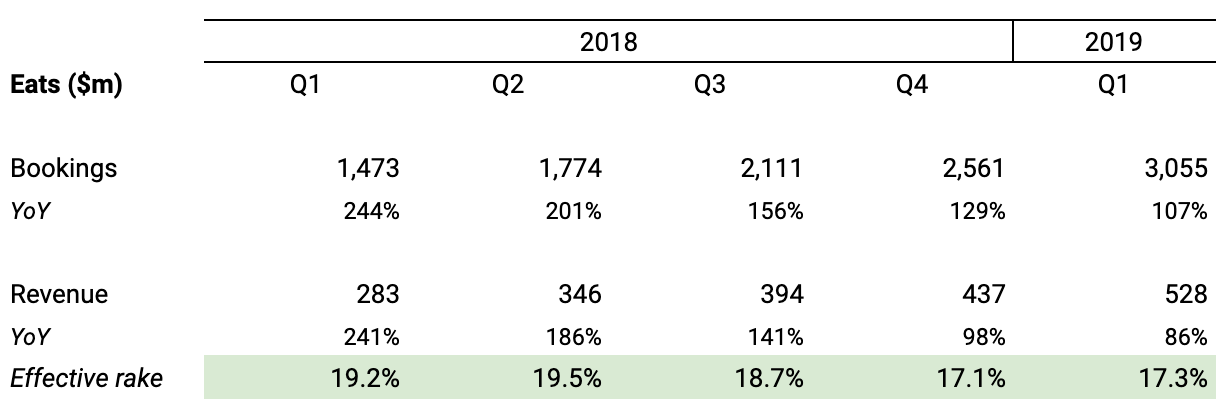

Eats, continues to be a big growth engine for the company, having effectively doubled revenues year-over-year as at Q1’19. The company clearly feel they can continue to extend the reach of Eats, to date, 15 million out of a total 91 million platform customers have used the product, headroom for growth.

Freight — Uber are also taking on the highly fragmented and inefficient freight industry. Their product looks to reduces friction in logistics by providing an on-demand platform to automate logistics transactions end-to-end. Until March of this year, Freight only operated in the US, though they have newly entered the European market.

Whilst, the company hasn’t provided line item details on P&L, we know that they did $359m of gross bookings in 2018 — a tepid start in comparison to the overall freight brokerage market in the US ($72bn), or even gross bookings of Ridesharing or Eats.

Aggregated topline numbers;

- the company booked $41.4bn in gross bookings in 2018

- this translated to $9.2bn in revenues, with a 22% blended take rate

The Future

As of today, Uber is firmly top of funnel for many urbanites looking to get from A to B conveniently and cost effectively. This places them, arguably alongside Google (Maps), in a valuable position in the smartphone-first urban transportation value chain.

Growth — Uber’s strategic growth prospects can be summarised as such;

leverage platform size x (doubling down on existing markets + new products)

This translates to; increasing rideshare penetration in existing markets, expanding light electric vehicles in new markets, expanding multi-modal capacities, continuing to expand Eats and Freight and investing in autonomous vehicles. Let’s dig into how:

Multi-Modal — In a post-Dara world, Uber has been active in placing itself as not only a transport network operator but also an aggregator of third-party transportation services. Strategically, this makes sense; exerting the power of its user base, extracting a platform tax whilst not dealing with the complexity of operating a transportation network makes sense.

“We plan to introduce multi-modal trips, a combination of our Ridesharing products, our New Mobility products, or public transportation, to create an optimal route for a consumer that can be more affordable than routes that do not incorporate public transportation.”

— Uber S1

If Uber can continue to add both public and private transportation networks to their platform, this will be a powerful consumer proposition. Whilst, going multi-modal seemingly isn’t optimising for short-term topline growth, Uber clearly understand the power of their platform and the value in being a significant player in large adjacent transportation markets.

Multi-modality makes sense for a number of reasons, though may also allow Uber to generate significant data around city-level transportation — the effective bundling of these services will allow Uber to down into monthly subscription packages, such as the newly launched RidePass. This potentially provides the company with more valuable, predictable recurring revenue and consumers, with all you can eat transportation.

Light-electric vehicles — 2018 was the year in which Uber really doubled down its effort into light electric vehicles, eBikes and eScooters, in order to target the majority of urban vehicle miles travelled, which is under 3 miles

Uber is in part responding to micromobility insurgents such as VOI, Bird and Lime, and also clearly view this as a short-term threat to core revenues and an attractive mid to long term growth opportunity. Clearly the company has taken the view that if anyone cannibalises these revenues, it should be them who do so. The disruptor highlights how its going to get disrupted;

“We believe that dockless e-bikes and e-scooters address many of these use cases and will replace a portion of these vehicle trips over time, particularly in urban environments that suffer from substantial traffic during peak commuting hours.”

— Uber S1

They’ve expanded this offering through a number of initiatives such as the $200m acquisition of Jump Bikes, the opening of a Chinese office to manage physical inventory supply chain and pushing light electric vehicles through their app to users in relevant geographies. As at year-end 2018, Uber owned and operated eBikes in 12 cities and eScooters in 4 cities.

Autonomous Vehicles — The companies’ historic struggles with unit economics, more specifically at the driver COGS level, led, in part, to forming Uber ATG (autonomous vehicles group) and the $600m acquisition of autonomous trucking company Otto. Today, both unit economics and profitability remain an outstanding question. Whilst the subject of autonomy has been significantly downgraded in importance;

“Along the way to a potential future autonomous vehicle world, we believe that there will be a long period of hybrid autonomy, in which autonomous vehicles will be deployed gradually against specific use cases while drivers continue to serve most consumer demand. As we solve specific autonomous use cases, we will deploy autonomous vehicles against them.”

— Uber S1

As evidenced with Waymo, we’re seeing the most plausible large scale go-to-market for autonomous vehicles to be ridesharing, in ring-fenced geographies. Unfortunately for Uber, the reality of autonomous has been slower than hoped. Uber spent $457m on R&D for ATG in 2018, and currently has partnerships with OEMs such as Toyota, Daimler and Volvo.

Unfortunately for Uber, Lyft has a close partnership with Waymo who have been aggressive in chasing down the opportunity in AVs. Uber’s autonomous program was paused last year by the tragic death of a pedestrian, whilst testing their autonomous vehicles in Tempe, Arizona. Whilst, autonomous remains in the narrative, the company have clearly accepted that’s unlikely to be a short to mid-term driver of growth or margins.

Conclusion

From a pricing standpoint, its difficult to assess the company with such a lack of tangible data such as CAC, ARPU and retention — though the company is pricing at a relatively reasonable price-to-sales ratio, if using Lyft as a benchmark. Event though short-term operating profitability might be a way off, if they can lower their cost of capital and continue to find some scalability from their fixed cost base, fundamentals should improve. More interestingly, strategically the companies’ prospects remain attractive, as any industry leading insurgent in a market as large as transportation would expect. Its likely the company will be, one of ,if not the, dominant global transportation marketplace, further buoyed by high intent user end-points touching into retail restaurants and logistics.

Sam

We’re passionate about mobility here at Project A — if you’re building the next big company in the space, please get at me [email protected]